Germany is the ideal-typical trading state (Rosencrance 1986) focused on the pursuit of its economic interests and prosperity. The rise of German economic power over the past few decades means that Germany is increasingly able to call the shots and fashion the European political economy in its own image. Both increased power and economic success have made it more inclined to be less consensus-oriented. Domestically, economic interest coalitions benefiting from a comparative advantage have dominated German foreign economic policy, as they have in the past in other countries (Zakaria 1999, Narizny 2007).

The alignment of government, corporate and electorate due to Germany’s export openness and trade openness create a significant consensus with regard to policies, the recent political rise of a far-right-wing party notwithstanding. A successful and growing export sector will become economically and politically more powerful. After all, once economic growth and domestic employment have become more sensitive to economic-financial instability in Germany’s major trading partners, incentives do stabilize these economies increase. Path dependency is at work here, mediated through raison d’état type strategic as well as domestic economic interests. It is the congruence of these interests that has allowed Germany put in place a substantial financial support. There are few examples in history where a government has committed this amount of resources to help stabilize other countries.

German power, initially largely structural and later largely relational in nature, provides Berlin with considerable influence to shape inter-governmental and supra-national governance reform in Europe. Obviously and tellingly, its influence is greater vis-à-vis Eurozone members than countries outside the Eurozone (e.g. UK) and its influence is greater vis-à-vis fiscally weaker countries than fiscal stronger countries (e.g. Finland). Eurozone membership imposes important constraints on countries and this strengthens the influence of the financially and economically soundest among the large economies: Germany.

|

| Source: OECD *domestic value-added (% gross exports) x exports (% GDP) |

German power, initially largely structural and later largely relational in nature, provides Berlin with considerable influence to shape inter-governmental and supra-national governance reform in Europe. Obviously and tellingly, its influence is greater vis-à-vis Eurozone members than countries outside the Eurozone (e.g. UK) and its influence is greater vis-à-vis fiscally weaker countries than fiscal stronger countries (e.g. Finland). Eurozone membership imposes important constraints on countries and this strengthens the influence of the financially and economically soundest among the large economies: Germany.

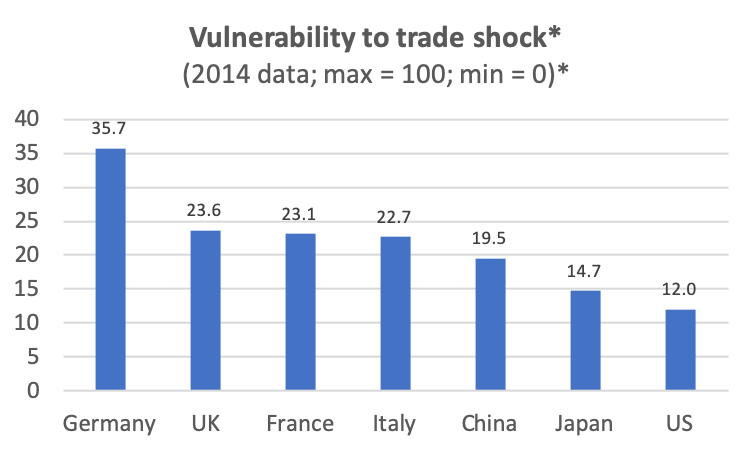

Historically, Germany has been very trade-dependent in terms of exports of tech-intensive goods and the import of raw material to sustain its industrial sector. German prosperity is highly dependent on access to foreign markets. Germany is therefore interested in trade and mitigating its trade dependence. It cannot afford prolonged economic instability among its major trading partners. It cannot even afford instability in a smaller country (e.g. Greece) given the economic and financial inter-connectedness characterizing the Eurozone. A sovereign default, let alone a Eurozone exit of one or several of the smaller countries could have the potential to destabilize the entire Eurozone. A sovereign default followed by a Eurozone exit could lead to the reintroduction of capital controls and, in extremis, trade protectionism. In short, instability in even a small economy carries the risk of large-scale systemic instability and represents a potential threat to the Common Market. Germany is concerned about potential systemic instability as much (or more) as it is about the direct consequences of a sovereign-default-cum-exit, which would force the German government to bail out parts of its financial system. It is therefore imperative from the German point of view to prevent such a scenario from materializing or, if this turns out to be impossible, to manage it in a way as to prevent a systemic collapse.

First, European economic integration guarantees Germany access to important foreign markets in terms of trade and investment. EMU consolidated this further by locking in the exchange rate of many of its major trading partners, thus furthering cross border trade and investment and preventing trading partners from devaluing their currencies and thus from offsetting German competitiveness. Moreover, EMU reflected almost exclusively German preferences and interests (e.g. low inflation, institutional independence, government financing), allowing German industry to do rather better than its less ‘adapted’ fellow Eurozone members.

Second, Germany has a large export sector adjusted for its economic size. Structurally, a large export sector creating high-wage employment gives export interests even greater political sway. It also creates incentives for the government to make a major effort to save the Eurozone given the implications of continued instability, let alone a break-up for German growth, employment and ultimately economic stability.

Third, Germany’s long-standing specialization in high-valued-added, technology-intensive capital goods provides further incentives to maintain export markets. While standard economic theory suggests that free trade is always welfare enhancing, it is easy to see how the expansion of high-value-added, tech-intensive industries is particularly attractive, given its tendency to generate large profits and high wages, thus benefiting German welfare.

Leaving aside broader political considerations, it is in Germany’s economic fundamental interest to stabilize and preserve the EMU. Naturally, it would like to achieve this while limiting its financial risk and/ or by limiting the financial subsidy, whichever form it may take (e.g. below-market interest rates, financial guarantees, permanent fiscal transfers), it provides. It therefore supports conditional, subsidized (multilateral) financial support in exchange for economic policy and structural reforms. It is conditional in that it seeks to tighten and enforce more readily fiscal and public debt targets with the aim of getting its money back, avoiding future instability and limiting the risks to its financial position. By doing so, it makes economic and financial adjustment and sustainability the responsibility of individual countries, albeit while supporting the adjustment through conditional financial support.